Third-Party Documents Alone? Not Enough for a Tax Demand.

Can the Income Tax Department raise a tax demand merely because your name appears in someone else's documents?

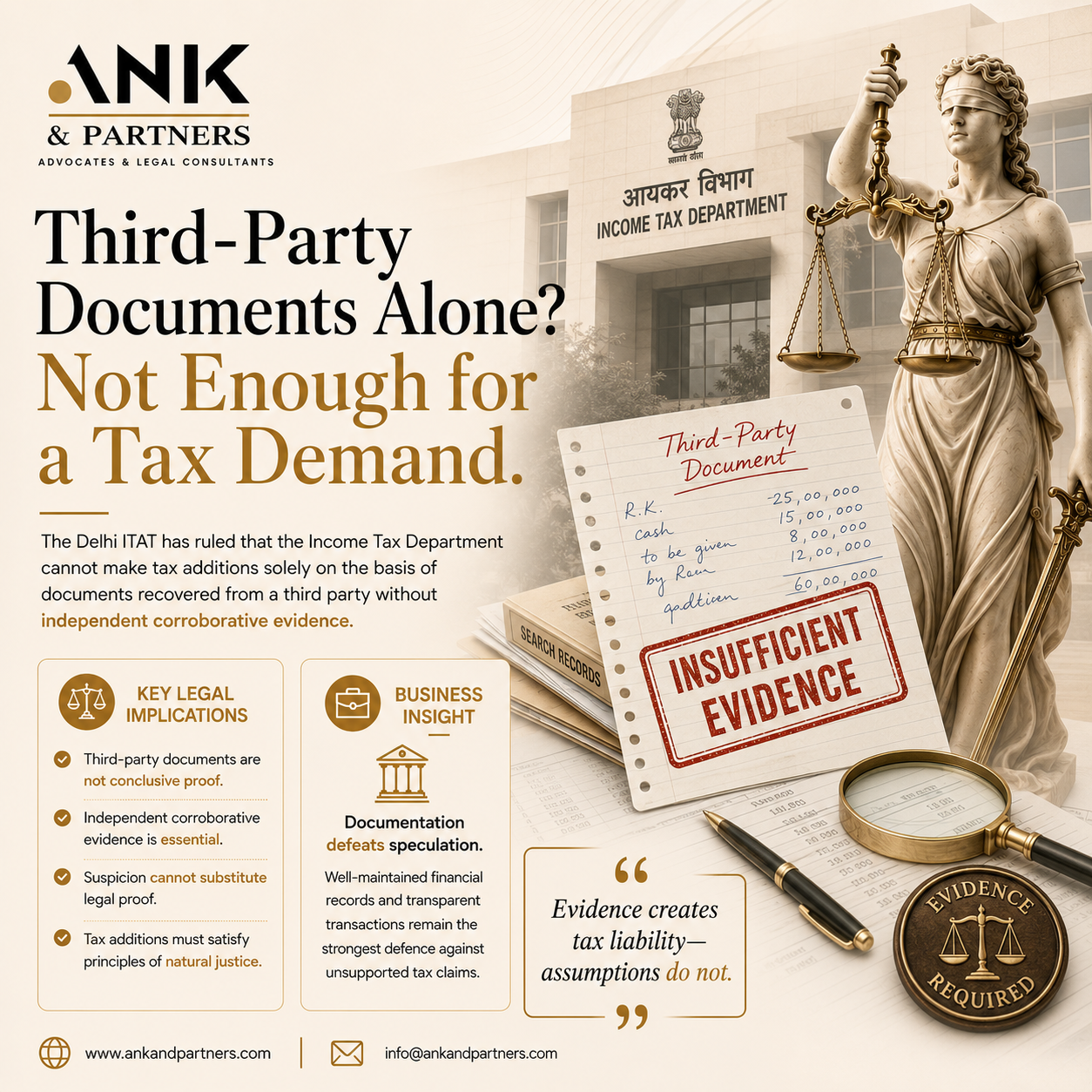

The Delhi Bench of the Income Tax Appellate Tribunal (ITAT) has reiterated an important principle of tax jurisprudence: No.

In Dolly Sabharwal v. DCIT, the Tribunal held that a loose sheet or handwritten document recovered during a search on a third party cannot, by itself, justify an addition to a taxpayer's income. The Income Tax Department must establish the alleged transaction through independent corroborative evidence before making a tax demand.

Key Takeaways

• Third-party documents may justify an investigation, but they are not conclusive evidence.

• Tax additions cannot rest solely on unverified handwritten notes or loose sheets.

• Independent evidence—such as bank records, accounting entries, cash trails, or other corroborative material—is necessary to establish undisclosed income.

• The presumptions under Sections 132(4A) and 292C generally apply only to the person from whose possession the documents were seized and cannot automatically be extended to another taxpayer.

Business & Compliance Perspective

The ruling reinforces a fundamental principle of tax administration:

Suspicion may justify inquiry, but it cannot replace evidence.

Businesses and taxpayers should maintain robust documentation, as proper records remain the strongest defence against unsupported tax additions.

Takeaway

"Tax demands must be founded on evidence—not merely on someone else's paperwork."