Accommodation Entry Loans Treated as Unexplained Credit: ITAT Upholds Addition & Interest Disallowance

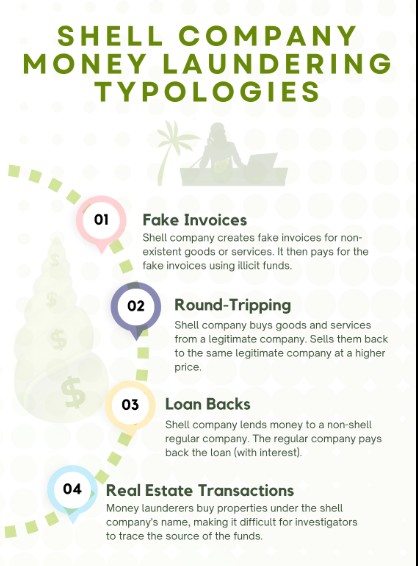

The Income Tax Appellate Tribunal (ITAT), Mumbai Bench, has held that loans obtained through accommodation entry providers constitute unexplained credit under Section 68 of the Income Tax Act, thereby upholding the addition along with disallowance of related interest expenditure. In the case, the assessee received a loan of ₹20.52 lakh from a lender later found to be a shell company engaged in providing bogus entries, as confirmed by its controller. Although the assessee produced bank statements and supporting documents to establish the genuineness of the transaction, the Tribunal held that the burden of proof was not discharged, especially in light of investigative findings and admissions regarding the lender’s lack of real business activity. The ITAT clarified that while Section 69A may have been incorrectly invoked, the addition was sustainable under Section 68 as the issue pertained to unexplained credit entries in the books. Consequently, the Tribunal upheld not only the addition of the loan amount but also the estimated commission and disallowance of interest, reinforcing that transactions lacking commercial substance and involving accommodation entries will attract strict tax consequences.